Fintech has been disrupting the banking industry by redefining new ways of banking as opposed to the old ways of traditional banking.In the 1990s, Bill Gates said: "Banking is necessary, banks are not" and this statement rings even more true this day as evident by the continuous rise of fintech disrupting traditional banking.

How and Why Has Fintech Disrupted The Banking Industry?

KPMG reports that in 2019, global fintech investment came up to a total of $135.7 billion and predicts that 2020 will be another big year for fintech, especially with the ongoing evolution of AI and blockchain. With the pandemic, online-only banking services are also seeing growing demands from consumers. [caption id="attachment_1212" align="aligncenter" width="812"]

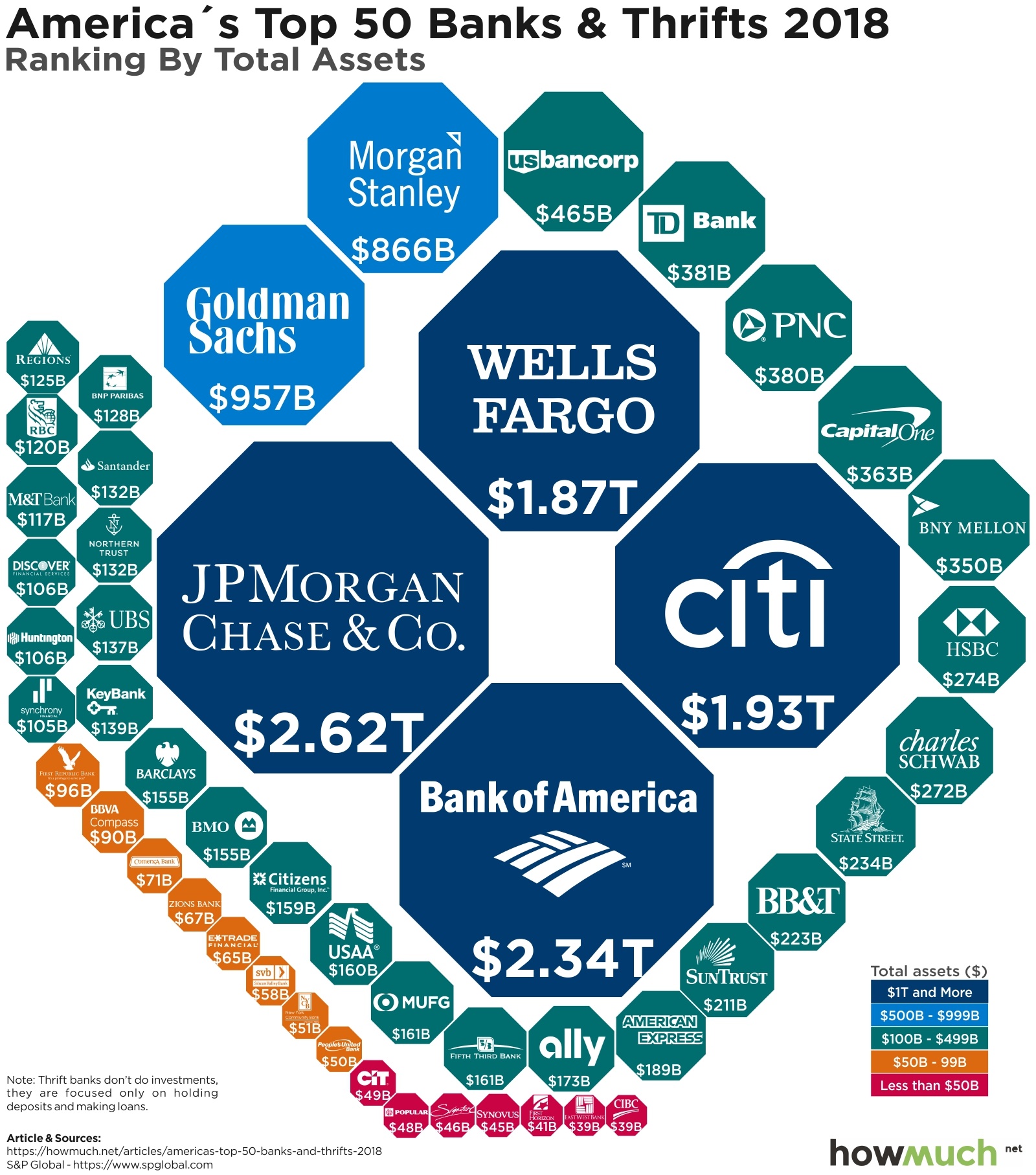

Credit: https://assets.kpmg/content/dam/kpmg/xx/pdf/2020/02/pulse-of-fintech-h2-2019.pdf[/caption]Comparatively, traditional banks such as JPMorgan Chase & Co. spend more than 10% of their yearly revenue on technology. What do these numbers look like? Forbes reports that JPMorgan Chase & Co. had allocated $11.4 billion for their technology budget in 2019, which has increased by 5.6% from its budget of $10.8 billion in 2018.It's important to note that the biggest traditional banks control a huge majority of assets, American banks alone control up to $17 trillion in assets, which is ginormous compared to fintech.[caption id="attachment_1213" align="aligncenter" width="1600"]

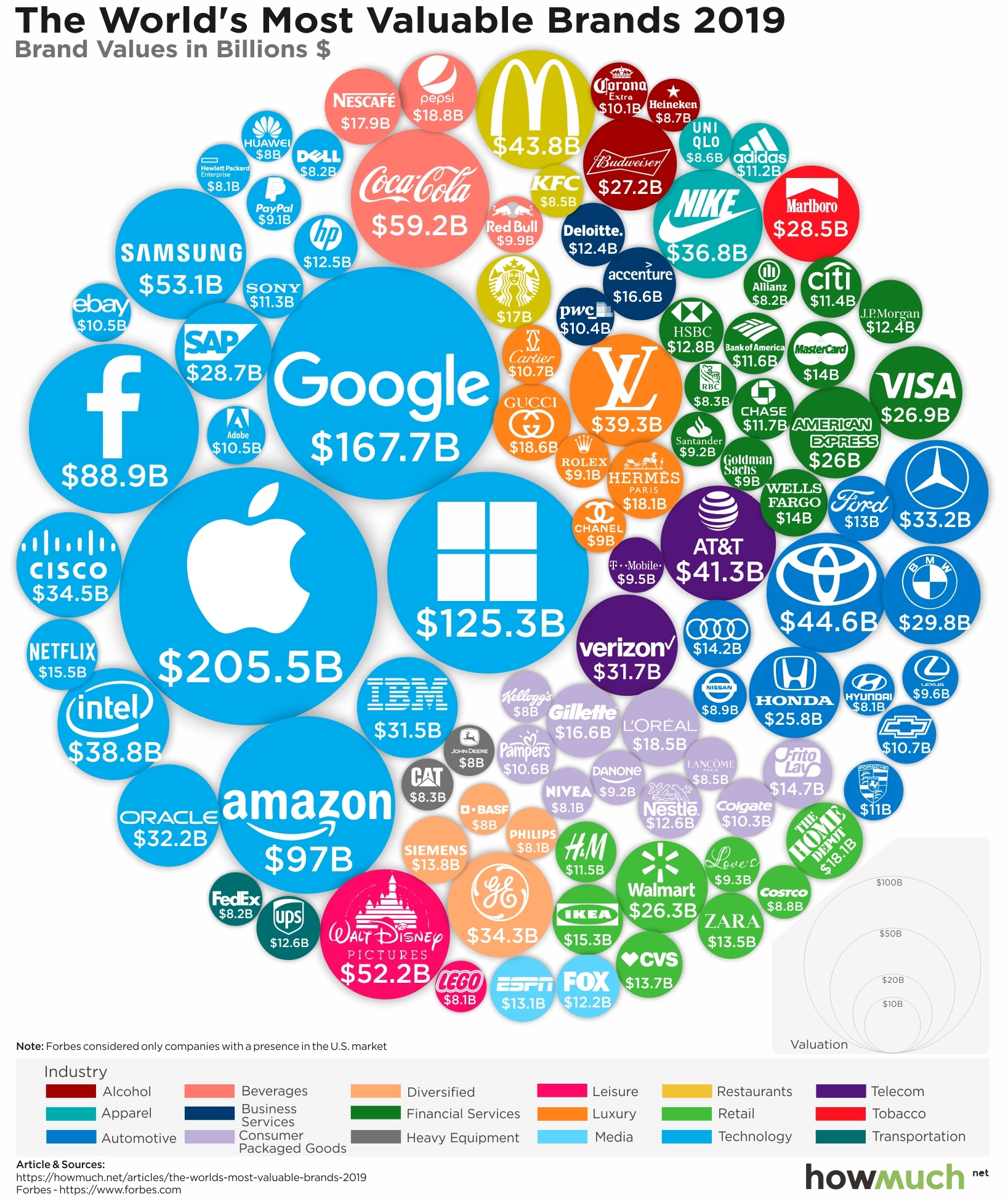

Credit: https://howmuch.net/articles/americas-top-50-banks-and-thrifts-2018[/caption]It's evident that technology, whether traditional or fintech, is being heavily invested in. However, there's something important to point out: Bloomberg reports that 50% of the digital transformation spent from traditional banks is wasted.Traditional banks have been trying to catch up to the surge of fintech companies, it doesn't help that traditional bank managers are resistant to change and new technologies. Their technological improvements through the years aren't done with their customers’ experience in mind but more for profit.The transition to online banking is a strategic move and it's a transition that has been made because it's beneficial for the profit of banks. The cost to maintain an online banking system is much less compared to the cost of maintaining physical branches.Comparing this to fintech, in which the fintech revolution sparked during the financial crisis in 2007-2008, paved a new way where finance teamed up with IT to create fintech startups to solve problems for people instead of banks.This is the biggest factor in the disruption: instead of strategising for banks, the fintech sector strategises for the people/end user. Not to mention, during the economic crisis, the trust that people had in traditional banks were broken creating a golden opportunity for the digital industry, kickstarting user-centred financial services.The digital age we live in now has uncovered countless opportunities for fintech, especially with the sweeping current of contactless payment and eWallets that isn't just popular but necessary during the Covid-19 global pandemic.If we take a look at the world's top 100 most valuable brands, we see 5 tech giants dominating, and the common denominator? They are user-centric in delivering positive user experience. This is what the digital age requires, and this is where the money really is.[caption id="attachment_1214" align="aligncenter" width="1637"]

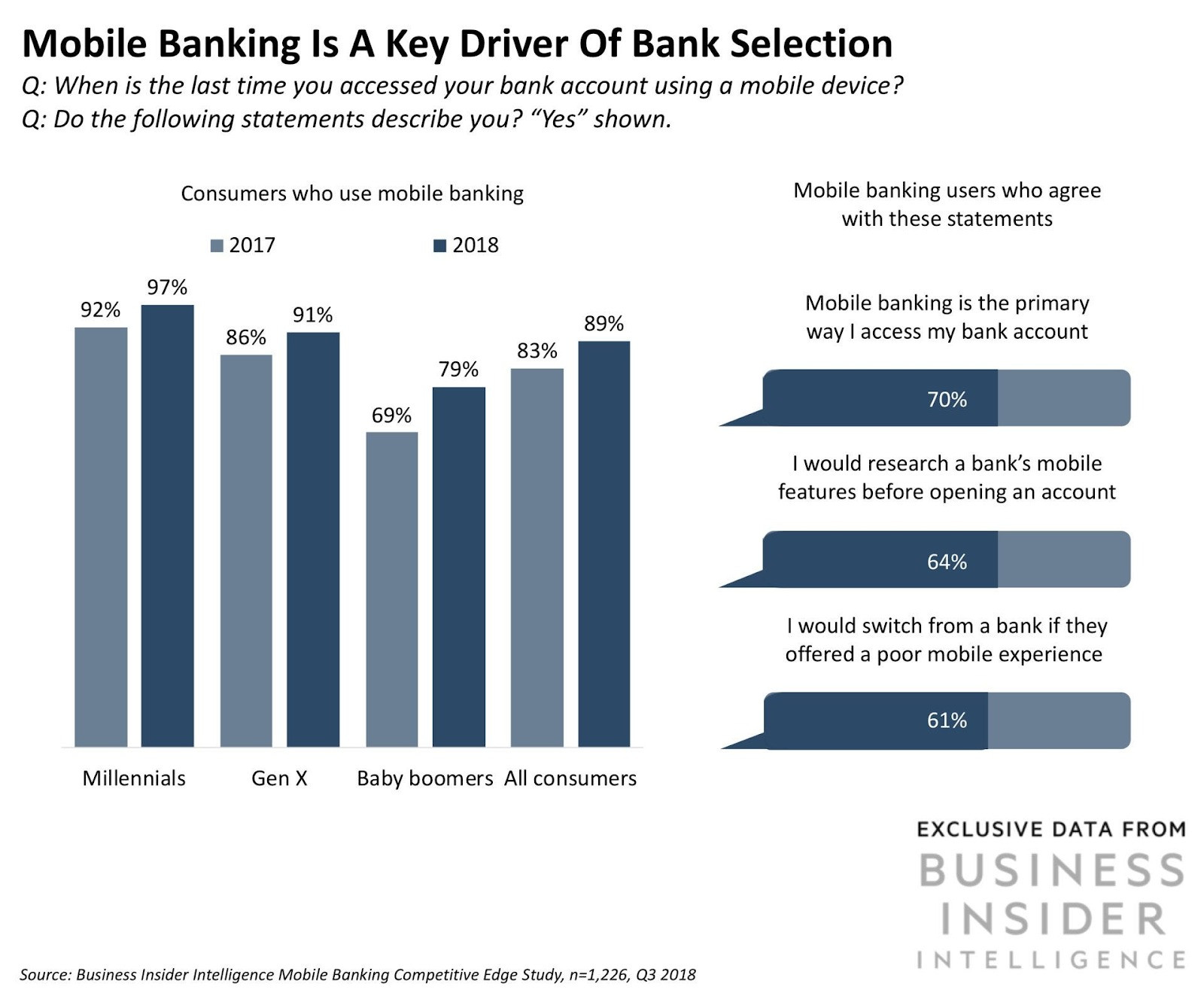

Credit: https://howmuch.net/articles/the-worlds-most-valuable-brands-2019[/caption]Comparing the sky blue colour of the technology industry to the deep green colour of the financial services industry, it's clearly evident that the technology industry is much higher valued. Not to mention, the 2 biggest of 5 tech giants, Google and Apple, have their own fintech services: Google Pay and Apple Pay.Mobile banking creates a demand regardless of location, eliminating market entry barriers. According to Business Insider Intelligence's Mobile Banking Competitive Edge Study in 2018, 89% of all consumers use mobile banking, and a whopping 97% of millennials use mobile banking.

Remaining up-to-speed on mobile market trends is crucial in attracting and maintaining customers, and fintech is doing well in providing these solutions to banking customers, allowing them to be competitive with traditional banks.

How Has Fintech Won over Customers?

The fintech revolution was led by those who understood the significance of design thinking, customer-centric solutions and thus created these services where banks have struggled. As a result, we have better finance management tools, various eWallets, mobile payments, and even Insurtech (insurance technology) solutions.This is all because fintech innovators put their customers first, took the time to understand their customers in the real struggles they faced in banking services through user experience research.Banks have tried to come out with their own digital solutions, but unfortunately, they tend to be overly complex with confusing user interfaces. Comparing this to the user-friendly interfaces of fintech solutions where they place an importance on creating a delightful user experience, it's a no-brainer why customers would prefer to use something that makes their lives easier.Fintech has won over customers because they have tried to see and craft their digital service FOR customers, choosing to place their customers first and creating products customers want to use. They also constantly user test their design to monitor the usability of their website or app user interface.On the other hand, traditional banks place their focus on better loan solutions, decreasing fees and convenient branch locations but customers want accessibility, simplicity and comfort.It's not to say that banks aren't offering services that fintech companies are, take personal finance management tools for example. Almost all banks have them but they are so hard to find and even harder to use! Customers will invariably prefer to download a new app on their phone where the app is easier to use instead of trying to figure out how to use the existing complex solution from the bank.Let's see how customers compare traditional banks with fintech on Google Play:

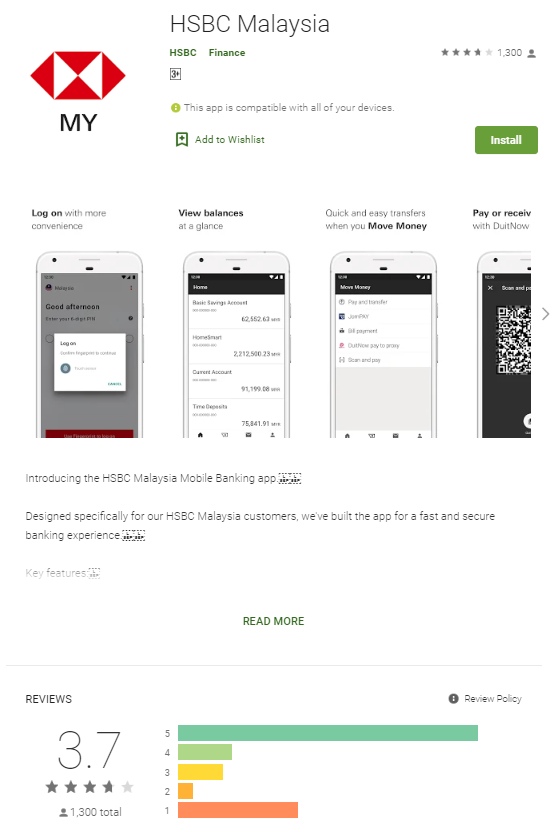

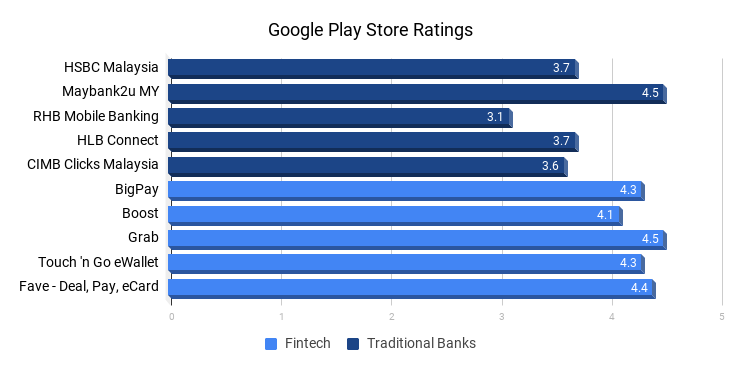

The HSBC Malaysia mobile app has a 3.7 rating from a total of 1,300 users

BigPay mobile app has a 4.3 rating from a total of 13,294 usersThe difference of 1,300 users compared to 13,294 users speaks volumes, fintech solutions are easily winning over customers.[caption id="attachment_1241" align="aligncenter" width="741"]

*Ratings obtained from Google Play Store as of 3rd August 2020[/caption]In comparing the top 5 traditional banks vs top 5 fintech companies in Malaysia, the bar chart clearly shows that the star ratings for fintech companies are all beyond the 4 star rating whereas only 1 out of 5 traditional banks is rated higher than 4 stars.

What Can Banks Do?

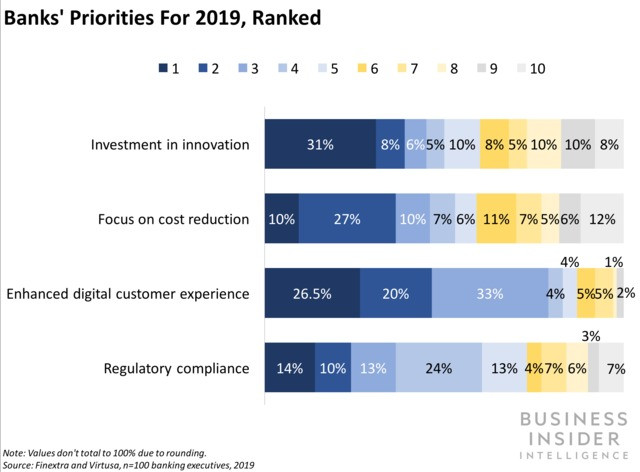

The concept of banking has been around since the time of the Roman Empire and will continue to be around, banks are not going to disappear but there's a need to embrace change and adapt in order to survive. The challenge to embrace is to shift to thinking and creating for customers and delivering a pleasant user experience.According to Business Insider, in a survey they conducted with over 100 banking executives throughout North American, Europe and Asia Pacific, digital customer experience is the top priority for 79% of the respondents.

Digital customer experience or user experience is vital in keeping up with the digital age, it poses a challenge to traditional banks in changing operating models and culture that has been around for so long. The shift to approaching services with the customer at the heart needs to be made in order to deliver financial services that customers would use and enjoy.The expectations are higher than ever, technology is ever-changing and evolving at high speed. Financial institutions, financial service companies and banks need to innovate in order to retain their existing customers and attract new ones, this could be in the form of personalized experiences across multiple channels. Design thinking is one of the best ways to solve this, but not only in the processes but at the very culture of the company.Fintech is shiny and new, and customers have the freedom to switch banks easily. Some fintech companies are also developing allowing consumers to connect different bank accounts to the same platform, making it easier for consumers to consolidate and view all their finances in one place. Banks should put the customer at the centre and revolve everything around that concept. Having great online services that are easy to use is a good step in the right direction.In fact, traditional banks and finance companies are collaborating with fintech companies in integrating them into their own ecosystem. This is a great way to stimulate innovation and in implementing fintech UX design.In order to meet the expectation of their customers, banks should look beyond the traditional ways of banking. Collaborating with fintech, UX consultants, user experience researchers & design professionals who are experts in understanding customers' needs, wants and expectations will help banks better deliver customer-centric digital solutions.

Summary

A combination of these strategies can help banks to compete with fintech disruptors in the future banking industry:

- Embrace change and adapt, update operating models and culture

- Customer-centric: shift to thinking and creating for customers at the heart

- Aim to deliver a pleasant user experience for your customers

- Invest in user experience research and usability testing to validate their digital service really meets end-user expectation

- Collaborate with fintech, UX consultants, user experience researchers & design professionals